The Hope Index 2023

A quick glance at the news each day often suggests there is little to feel hopeful about in spring 2023: continued conflict in Europe fuelling a cost-of-living crisis, public services overstretched and understaffed, ‘final warnings’ from scientists about the climate emergency, political instability at home and abroad and an often fractious culture war.

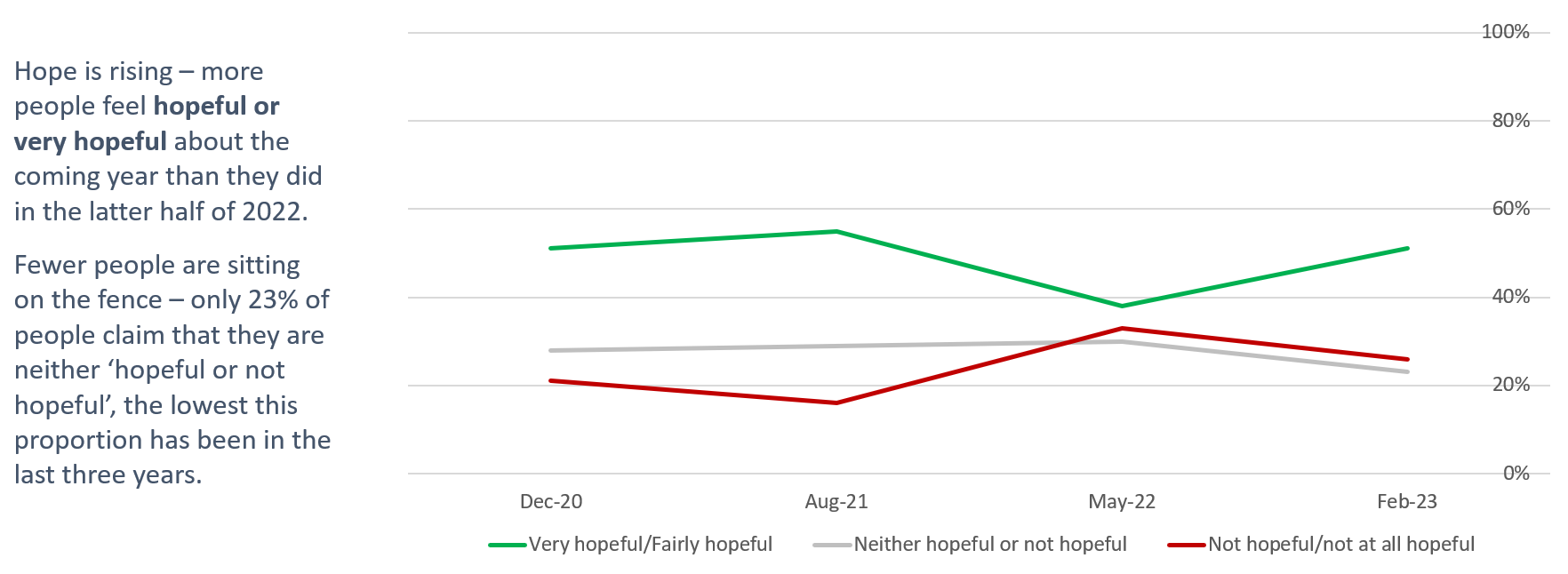

And yet, in the third year of our extensive research, we find that hope among the public is on the rise.

Field research from a nationally representative sample of over eight thousand respondents - much larger than most comparable surveys - has suggested hope for the future has bounced back from the sub-40% lows of Autumn 2022 to 51%. This increase is consistent across a number of different question areas, suggesting this optimism is more than just the ‘spring effect’.

The level of public hopefulness has returned to that we saw during the pandemic, when our research found a sense of national togetherness drove increased hope in spite of the challenges we faced. And in this survey we observe some interesting trends:

Hope is felt more strongly by younger generations (under 44 years old) and those in urban areas.

45–64-year-olds were less hopeful – the age group that is undoubtedly facing the largest cost increases in terms of food, energy and mortgage costs with hiked interest rates.

Those 44 years old and younger are more likely to be concerned about issues including mental health and climate change, while older generations are more likely to focus on social care and immigration.

There are higher levels of hopefulness at every income level – though hope naturally soars among the most wealthy.

Domestic considerations are front of mind, with the war in Ukraine falling down the priority order compared to our findings last year.

At the same time, while concern about the economy and cost of living remains high compared to last year – concerns about the introduction of new taxes and energy security have been replaced by a focus on the NHS and corruption in politics.

While climate change appears lower as a priority in our quantitative research, our focus groups revealed it remains front of mind as a concern for the majority of people we spoke to.

The results of the Hope Index should not be overstated: serious challenges remain both at home and abroad. But it provides further evidence that in fact the public are more confident about the year ahead than public and political debate might suggest. During our focus groups our participants often commented that they believed the UK would recover from its current economic challenges, recalling the recovery post-2008 as their proof for this view.

This short report is the first publication in a series from this extensive research programme. Later in April we will publish new evidence showing how companies can act to earn reputation, followed by further insights into the growing UK age-divide and those which demonstrate the Leave/Remain voter divides may now have closed for good. If you would like to discuss this research and our work in more detail, please email hello@5654.co.uk

As we emerge from winter, we are more hopeful

Q: Thinking about your own life, and the things that shape it, how hopeful are you about the coming year?

8043 respondents. Fieldwork: 10 Feb 2023 - 17 Feb 2023

Hope is higher among younger people and city dwellers

A larger proportion of 45-64 year olds are not hopeful about the coming year compared to younger groups. A significantly higher proportion of those living in a city would agree that they are very hopeful about the coming year, compared to those living in a town or village.

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

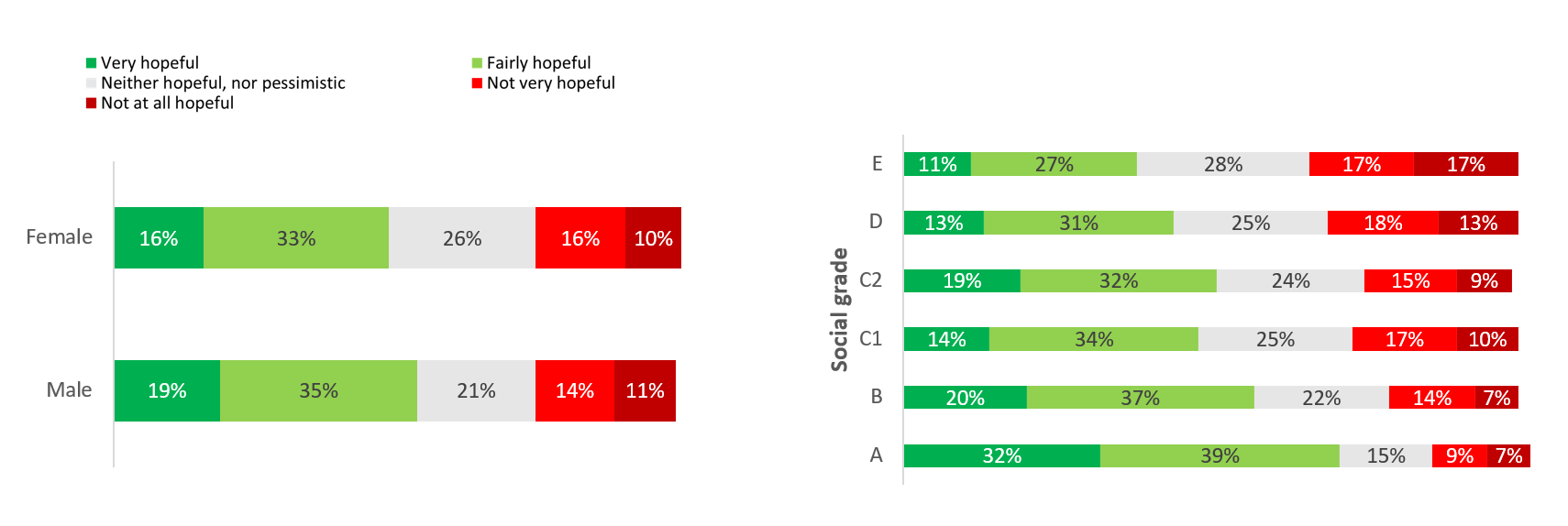

The public are hopeful almost regardless of their income, while men are slightly more hopeful than women

The public’s level of hopefulness is consistent across social grades – except for the most wealthy where hope soars. Men are also slightly more likely to be hopeful than women, with 54% claiming they are either hopeful or very hopeful (compared to 49% of women).

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

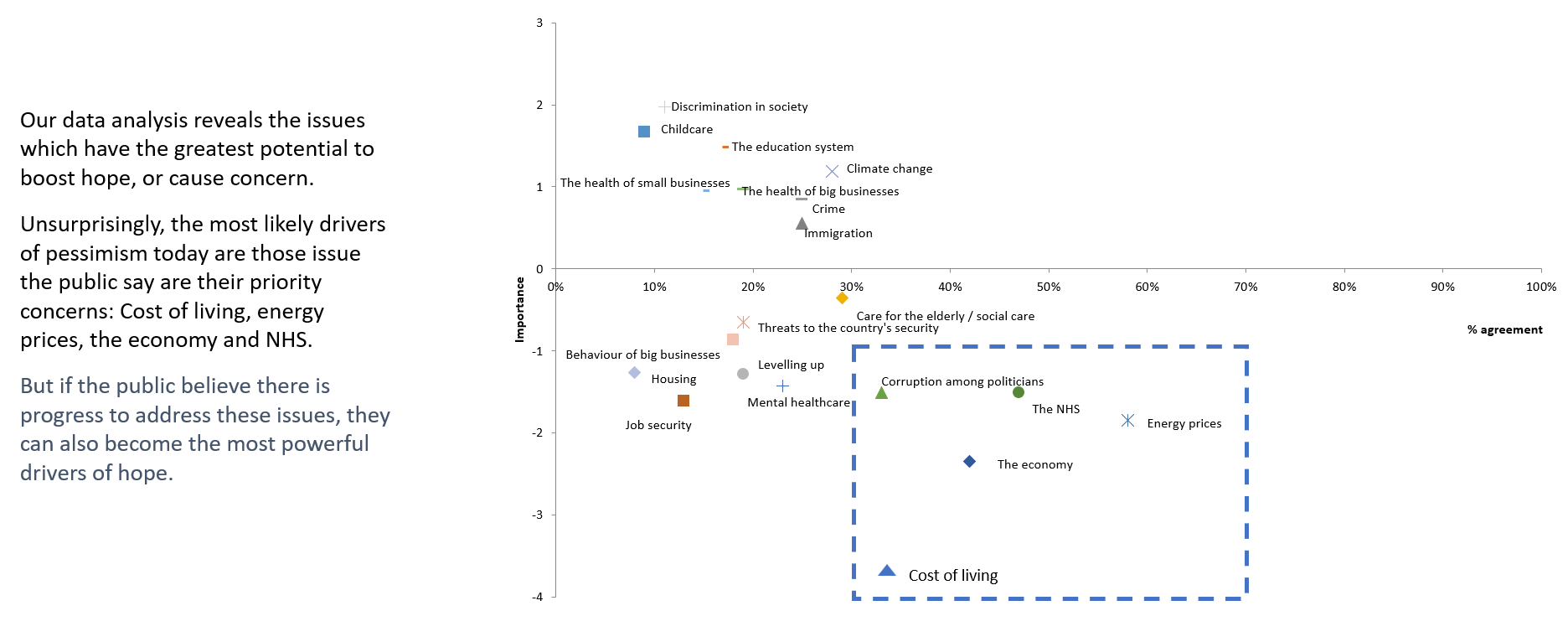

The public are most worried about the cost of living, energy prices, the economy and the NHS

More than half of respondents said they are very worried about energy prices and the cost of living crisis – and the vast majority say they are either worried or very worried. Nearly half of respondents are very worried about the NHS and the economy.

Corruption among politicians is also a top concern – 63% of respondents said they were worried or very worried about it. When it comes to lowest priority, a third or more of respondents are not very worried about housing and job security. These findings were reflected in focus groups we ran during February which revealed the public are concerned about ‘the next generation getting on the housing ladder’, but most often not about their own prospects. It was also notable in these groups that while concern about climate change features lower in these results – in our focus groups it was a topic raised as a priority among attendees in every discussion.

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

The top concerns are consistent across age groups

The public’s top three concerns – the cost of living, energy prices and the NHS – remain consistent across all age groups, while corruption among politicians and government is shared top concern for those aged 25 - 64. The NHS and access to social care are a greater priority for those 45 and older. And immigration features as a top concern for those over 65 years old while climate change appears as a priority for those aged 18-24.

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

Compared to last year, people’s concerns are closer to home

Compared to our findings last year, the public continue to be worried about the cost of living crisis and energy prices. But the NHS emerges as a new priority. And there has been a shift away from the international to the domestic, with geopolitical insecurity no longer a top public concern. This was also reflected in our focus groups, in which participants said they felt that the UK has been too focused on the war in Ukraine and not focused enough on ‘tackling problems at home’. Corruption among politicians and government also emerges as a new top concern – an issue which was raised regularly during our focus groups, and which was often cited as the reason the public say they are not currently interested in politics.

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

Delivering on the economy, energy prices and the NHS can boost hopefulness

8043 respondents

Fieldwork: 10 Feb 2023 - 17 Feb 2023

Methodology

Poll: We interviewed 8,043 British adults online between 10 February - 17 February 2023. The data is representative of the British adult population.

Focus Groups: We conducted focus groups in February to support our poll and collective qualitative insights into the publics priorities.

A note on our regression approach:

The above charts have narrowed down the statements we used in our regression analyses to those which were 'statistically significant' in driving hope.

We have taken the "Relative Importance" score from the regression model, as this gives us each statement's contribution to r-square (which is the number that tells us how well the data fits to our regression model i.e. strength of relationship), in percentage form.

This score is more resilient to relationships between the statements themselves than regression coefficients.

It is also worth noting that each regression was run more than once, with the second (and third and fourth) iteration removing the small pool of respondents who were providing 'bad data' (i.e. an algorithm was used to spot any non-logical responses, that would suggest low integrity in the respondents answers).

This gives us greater confidence in the "Relative Importance" scores for our statements, as it lifted the R-square number and ensured the relationship between the statements and ‘trust' were even stronger.